Image Description: On The Record 6-23-26. Greenspan Dead. Starmer Done. Elon Cooked. Altman F*cked. Housing Crushed. UNFTR.

Image Description: On The Record 6-23-26. Greenspan Dead. Starmer Done. Elon Cooked. Altman F*cked. Housing Crushed. UNFTR.

“Mumbling With Great Incoherence”

The great man has died. The all-knowing, all-powerful, and second longest tenured chair of the Federal Reserve has left this earthly plane, presumably to preside over God’s vast holdings and riches.

Part of what made Alan Greenspan perfect for the time he reigned (1987–2006) was his ability to, as he put it, master the art of “mumbling with great incoherence.” To the outside world, the “Maestro,” as he was known in The Beltway, Greenspan was the money whisperer. His judgment was never to be questioned. The bottom rung of the economic ladder was never counted against him so long as the gains at the top continued to grow unabated.

In addition to ushering in what many believed to be an era of prosperity, Greenspan ushered in an era of extreme secrecy at the Fed. His methods were not to be questioned, and he displayed very little patience for those who summoned him to testify on the Hill. He was no mere mortal and reviled being treated as such; thus the self-described tactic of mumbling incoherently. Why bother explaining things to the commoners?

But Greenspan wasn’t as much responsible for the wealth gains during his tenure as he was the reputational beneficiary of them. As Jeanna Smialek writes in her Fed book Limitless, “Greenspan’s cult of personality owed in part to the era he oversaw. He had been dealt a winning economic hand by history, presiding at a time of globalization hypercharged by a relatively young working-age population and big advances in computer technology, one in which laissez-faire economics and animal spirits were celebrated as engines of prosperity.”

Before Greenspan ever set foot inside the Federal Reserve, he spent years cultivating a very particular intellectual identity. He was a card-carrying disciple of Ayn Rand, a fixture in her inner circle of objectivists, absorbing the gospel that markets were self-correcting, that regulation was coercion, and that government interference in economic life was a moral failing. This was a man who genuinely believed the Federal Reserve—the very institution he would one day lead—was a philosophical abomination. The central bank, in the objectivist worldview, was the embodiment of everything wrong with statist interference. And yet, ambition has a way of softening one’s philosophical commitments.

What greased the skids for Greenspan’s entry into the corridors of power was a piece of work so cynically brilliant it almost demands admiration. In 1983, Ronald Reagan needed to shore up Social Security, as the program was hemorrhaging cash, but he could not be seen raising taxes. His entire political brand was built on the promise that taxes would go down, full stop. So Reagan commissioned a fix.

Enter Greenspan, who chaired the National Commission on Social Security Reform and engineered what can only be described as the perfect Washington parlor trick: raise payroll taxes dramatically on working Americans by increasing the Social Security deduction, while leaving the income cap in place. The wealthy would pay the same flat amount they always had. The burden fell squarely on the middle and working class. It was, in every functional sense, the largest tax increase in American history—packaged and sold as a solvency fix. No one called it a tax hike. Greenspan had his ticket punched.

For a man who professed to despise government, he proved remarkably comfortable inside it. He navigated Washington with the ease of a born insider, schmoozing, testifying, advising—the very definition of a Beltway gadfly—all while maintaining the posture of the reluctant technocrat called to serve. The Federal Reserve chairmanship, when it came in 1987, was the logical culmination of a decades-long project of making himself indispensable to the powerful.

For nearly two decades, it worked. The economy hummed, at least for the upper half of it. The markets rose. Greenspan spoke in riddles and the world leaned in to decode him. But beneath the surface, something was rotting. Throughout the early 2000s, as the housing bubble inflated to grotesque proportions, Greenspan actively encouraged American households to take on more debt: floating-rate mortgages, home equity lines of credit, adjustable-rate instruments that looked cheap in the short-term and became punishing traps when rates moved.

And rates did move. Because he fucking moved them. Greenspan raised the federal funds rate 17 consecutive times between 2004 and 2006. The households he had encouraged to stretch were now being slowly strangled by the same instrument he controlled. The over-leveraging of the American middle class was not an accident of markets. It had a facilitator.

Then came 2008. The whole architecture collapsed. And Greenspan sat before Congress and delivered what should have been a moment of reckoning. He admitted, with characteristic understatement, that he had “found a flaw” in his ideology. He had not accounted, he said, for the degree to which self-interest on Wall Street could be destructive rather than corrective. The market, it turned out, did not always know best. The lifetime of intellectual scaffolding he had constructed—the Randian framework, the objectivist faith in rational actors, the contempt for oversight—had a hole in it big enough to drive the global financial system through.

What followed was not contrition. It was a book. The Map and the Territory, published in 2013, offered Greenspan’s retrospective account of his career and the crisis. It gestured at uncertainty. It updated some models. It did not apologize. Rather, it suggested that more psychological and behavioral frameworks should be adopted instead of relying strictly on math and models. Not his behavior, or that of the political elite who would starve the masses to enrich the few. Everyone else’s “herd mentality.” That was the problem.

The Maestro had played a wrong note. Instead of admitting it, he simply rewrote the score.

The Housing Supply Reckoning

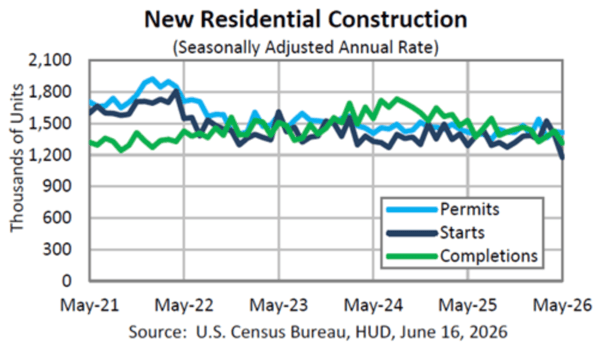

We did an extensive piece on housing a couple months ago showing how stuck the U.S. housing market is right now. High rates, high valuations, little movement. Since that time, things have changed only slightly, but May proved to be a particularly tough month. One thing to keep in mind with Census data is a pretty significant margin of error of around 9%. That said, the May housing starts number was outside of this range showing a 15.4% drop that hit like a 2x4 to the face. For context, this is the lowest reading since COVID. And it missed the Wall Street consensus by 230,000 units. Yikes.

Source: Census

The headline number is bad enough, but the real story is what happened in multifamily construction—buildings with five or more units, the apartment towers, and mid-rise developments that were supposed to be the supply-side answer to the nation’s housing crisis. Multifamily starts fell 40.2% in a single month, the steepest monthly drop since April 2009, when the financial system was in full meltdown mode.

Single-family starts dropped more modestly, down 1.9% from April to 882,000. Building permits, which signal future construction intent, were basically flat—down just 0.7% overall, with single-family permits actually ticking up 0.6%. So it’s not that developers have given up entirely. It’s that they can’t make the math work right now, particularly on the larger, more complex multifamily projects that require more capital, more materials, and more time to pencil out. This is the housing we need the most, so not a great signal.

It’s hard to ascribe blame to a single thing, especially in something as vital and broad as housing. Conditions vary from market to market so I think it’s best to examine the more universal forces. The most obvious one is mortgage rates. Irrespective of what our president says about lowering the Federal Funds Rate, I think it’s clear the market is setting the pace right now based on the health of the consumer. The 30-year fixed rate is still running around 6.4%, which isn’t problematic compared to prior decades but when you compare housing prices today versus ten, 20, 30 years ago it’s a major roadblock; especially for first-time buyers.

Rates and high valuations affect demand negatively for obvious reasons. But the bigger reason building might be holding off right now is because of tariffs. The Trump administration’s tariff regime has layered cost pressure onto an industry that was already stretched thin. Softwood lumber carries a 10% tariff. Kitchen cabinets and vanities are at 25%, and slated to climb to 50%. Steel and aluminum tariffs hit structural components throughout a build. Last year the National Association of Home Builders estimated these costs added $10,900 to the price of every new home. Even though many of these tariffs expired, they’re being re-upped through the temporary powers of the executive, so it’s hard to parse how much is impacting supply on a monthly basis.

When you put just these two pressures together, you get an affordability picture that’s genuinely grim. The median existing home price hit $429,300 in May, an all-time high for the month. National median family income sits at $106,800. A buyer putting 20% down at 6.48% is looking at a monthly mortgage payment of roughly $2,166, which consumes about 24% of that family’s gross monthly income. That’s before property taxes, insurance, or any maintenance.

Max is a political commentator and essayist who focuses on the intersection of American socioeconomic theory and politics in the modern era. He is the publisher of UNFTR Media and host of the popular Unf*cking the Republic® podcast and YouTube channel. Prior to founding UNFTR, Max spent fifteen years as a publisher and columnist in the alternative newsweekly industry and a decade in terrestrial radio. Max is also a regular contributor to the MeidasTouch Network where he covers the U.S. economy.