Image Description: On The Record 6-02-26. When the AI Bubble Will Pop. The Platner Problem. Shapiro Buys Views. Trump 250 Disaster. UNFTR

Image Description: On The Record 6-02-26. When the AI Bubble Will Pop. The Platner Problem. Shapiro Buys Views. Trump 250 Disaster. UNFTR

Economies of Scale

The most convincing argument against the AI economy that I’ve heard (and there are many) is that it breaks a fundamental economic law. Economies of scale. AI boosters have long said that the technology is in its infancy and will only continue to improve rapidly over time.

Moore’s Law, check.

Many industry leaders such as Sam Altman and Dario Amodei are beginning to reverse their claims that AI will displace the vast majority of jobs, and instead be closer to prior technological revolutions that created new opportunities at an even pace to displaced legacy roles.

Creative destruction, check.

But none of this compensates for the fact that for AI to improve and to create said opportunities, the cost structure over time grows commensurate with the technology. In other words, AI cannot deliver economies of scale. And this is a very big problem. The theory behind this is pretty straightforward. The larger the system, the more efficient it becomes to produce through a combination of buying power, distribution of unit costs and productivity that results from division of labor. The problem facing AI is that none of these factors are assumed under a core growth model. The bigger AI technology gets, the more expensive it is to produce. The fundamentals are completely upside down.

A lot of comparisons are drawn to the development of the internet. Massive investments into laying fiber and launching satellites didn’t pan out for the government and companies who made the primary investments. But as the internet matured, adoption increased and economies of scale took hold. In the internet economy of today we are all the beneficiaries of large scale government and corporate capital investments. It’s why the internet was compared to telecommunications, which was itself compared to the railroads before it. The first one in (usually the government) loses big. Second, loses less big. By the third, fourth and fifth generation of capital the whole thing kind of evens out then everyone gets paid back by the public equity markets.

Perhaps the most honest statement ever uttered by an OpenAI executive was when CFO Sarah Friar suggested that some sort of government backstop might eventually be part of the funding mix. Wall Street saw “backstop” for what it was: bailout. This quickly prompted founder Sam Altman to make the rounds online and on television to dismiss the idea. But if we think about the capital situation logically, this is what would need to happen to make this technology widely available, useful and affordable.

We’ve said for some time that AI was a lose-lose proposition absent government intervention. First off, in a world where the potential of AI is fully realized in the manner described by its progenitors, half of the country becomes unemployed. Their response to this has typically been that this is a net positive for society because productivity will itself boost GDP, leaving so very many of us with more time to write, garden, paint and generally fuck around. The implication being that we’ll all have a form of Universal Basic Income (UBI). Andrew Yang will be president and everything will be just fine.

Of course, no one stopped to think about what becomes of the people who perform non-technical services in this economy. If the UBI is enough for white collar unemployed people to live the life of Riley, then why wouldn’t everyone else just quit their jobs? And, of course, if the productive economy is fully automated and being run by agents developed by private firms, then all of the gains go to the corporate owners of the technology. Since corporations are taxed far less than individuals (percentage-wise and in absolute terms) then less money flows back into the government, which would necessitate an expansion of the domestic money supply. This would devalue the dollar and invite inflation and on and on and on. So, no. This isn’t well thought out.

But the bigger and more immediate issue is that under the same scenario of “success” we simply aren’t built to actualize it. As in, we don’t have the infrastructure to support the data center electricity and water needs required to guarantee adoption at a level to achieve economies of scale. Even in an “all things being equal” scenario where fossil fuel inputs are cheap (they’re not) and endlessly abundant (also not a thing), our electric grid and water distribution systems aren’t built to manage much more than we already have. And what we already have is producing some pretty bad economics.

Now factor in the fact that our fractured and aging energy grid runs almost entirely on inputs that are subject to massive price swings due to things like, I don’t know…a war in Iran, and the whole cost structure becomes a bit more tenuous. Of course, these centers also require a massive amount of both space and water. The problem here is that the areas with a lot of space don’t have enough water. And the places with water have a lot of people that need it to survive. Quite a conundrum.

If we really thought that AI was transformational in the way railroads, telecommunications and the internet were to the economy, then we would have gone about it in reverse. The grid would be modernized and upgraded to incorporate a wave of massive renewable and nuclear energy projects in largely unpopulated areas. They would be cooled by desalination plants and overbuilt to accommodate next generation chips and GPUs. As the older plants reached their useful lives, they would be recommissioned for the next generation and continue in this pattern. Data centers would be under strict regulatory supervision by a committee with representation from the departments of commerce, interior and energy and brought online gradually over several decades to allow enough time to turn over the labor market as the economy evolved. The regulatory framework would have strict prohibitions against military use cases and privacy and deepfake laws would be airtight.

And even this magical thinking scenario rests on the assumption that we have a clear understanding of what the fuck AI is even good for. (Still waiting for a clear answer on that one.) Don’t get me wrong, it’s neat. Does some stuff faster. Makes other things easier. But the industry has yet to pinpoint that one specific instance of clarity that shows us a different, better future. Saying that everything will just “get better and faster” doesn’t cut it.

It’s little wonder that AI is taking off during the age of Trump. The entire thing is propped up by “trust me, it’ll work out.” It’s all about the next press release and next FOMO investment opportunity. This year it’s the trio of IPOs—Anthropic, OpenAI and SpaceX—and I’m guessing this will be the last big puff into the bubble. None of these companies have revenue to support the outrageous valuations being floated. The one thing they all have in common, however, is a tremendous amount of early capital investments by major funders who stand to get it all back if all goes well.

With the exception of Elon Musk (see the KLTW) the early money investors need a huge opening, a flood of retail investors to ride the post-offering wave, and a sustained level of trading volume for the first year. And you can bet that as soon as their respective lockup periods end, they’ll head for the exits like rats on a sinking ship. That, my friends, is the real bailout. Not for the offering companies, they’re fairly well fucked. But for the early capital investors. Why wait for the government to make them whole with taxpayer money when they can just siphon it directly from your pension, 401(k) and Robinhood accounts?

Now that is market efficiency. But it ain’t economies of scale.

Actual Growth or Price Hedge?

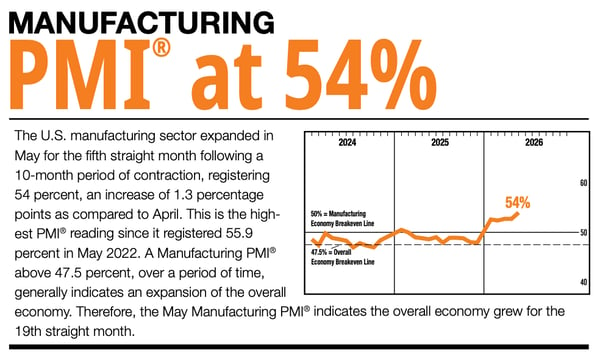

The recent ISM data showed a surprising uptick in manufacturing activity. And this time it’s pretty widespread, as opposed to previous indicators that seemed to show activity was limited to data center construction.

Source: ISM

Money continues to course through the economy, and it’s lifting the indicators in manufacturing. Attempting to pin down why exactly the figures are improving now is proving somewhat tricky. As Bloomberg notes, “The measure has now signaled expansion for five straight months, pointing to renewed vigor in the manufacturing sector amid a surge in artificial intelligence investment, more favorable tax provisions and diminished trade policy uncertainty.”

That’s one side, but the article continues saying, “Part of that strength may also reflect customers trying to stockpile merchandise in an effort to front-run future price hikes.”

-Jun-02-2026-02-05-44-0074-PM.png?width=1402&height=314&name=unnamed%20(1)-Jun-02-2026-02-05-44-0074-PM.png)

Most of the inputs point to a marginal uptick in activity, except for the price index, which is the biggest outlier. Despite the very recent downward trend in spot oil, which most observers don’t expect to hold, the fact is that prices have been increasing for all raw materials and are expected to continue this pattern. This is what gives more weight to the notion that a broad swath of the industrial economy is frontloading inventory again. This will be a crucial pattern to observe in the coming months.

Max is a political commentator and essayist who focuses on the intersection of American socioeconomic theory and politics in the modern era. He is the publisher of UNFTR Media and host of the popular Unf*cking the Republic® podcast and YouTube channel. Prior to founding UNFTR, Max spent fifteen years as a publisher and columnist in the alternative newsweekly industry and a decade in terrestrial radio. Max is also a regular contributor to the MeidasTouch Network where he covers the U.S. economy.