Image Description: On The Record 07-14-26. Graham Dies. McConnell Doesn’t. Elon and Sam Fight. June Budget Disaster. U.S. Nearly Out of Oil. UNFTR.

Image Description: On The Record 07-14-26. Graham Dies. McConnell Doesn’t. Elon and Sam Fight. June Budget Disaster. U.S. Nearly Out of Oil. UNFTR.

The Ledger Doesn’t Lie

Three-quarters of the way through fiscal year 2026, the Treasury Department dropped the June numbers on us, and if you want to know what a government actually believes—not what it says in press conferences, not what gets tweeted at 11 p.m.—you read its ledger. A budget is a moral document.

And the timing matters. The federal fiscal year runs October through September, which means October, November, and December of last year still had Biden’s fingerprints all over them—inherited appropriations, programs already in motion, the long tail of a prior administration’s choices bleeding into the first quarter of a new one. But by June, we’re nine months in. Tax season has closed its books, refunds have been processed, withholding patterns have normalized, and every dollar moving through this statement is a dollar Trump’s team chose to collect or chose to spend. This is no longer a transition document. This is his budget, in full.

So before we get into what it all means, let’s run through the highlights, because the top line numbers alone tell a story of contrasts; then we’re going to talk about debt, deficits, and the persistently false concept of fiscal responsibility that haunts us.

Let’s start with that framing: fiscal responsibility. It’s the buzzword both parties reach for when they want to sound serious, and it’s almost always deployed selectively—invoked to justify cutting a program for poor people, never invoked to question a supplemental for a defense contractor. Keep that in mind as we walk through what actually happened this year versus last.

The starkest split in this year’s numbers is on the receipts side, and it tells you plainly where this administration’s sympathies lie. Individual income tax receipts are up meaningfully year over year. Corporate income tax receipts, on the other hand, are down—and not just down, but down while corporate refunds simultaneously went up. What it means is the government is collecting more from paychecks and handing more back to boardrooms. If a household’s tax bill and a corporation’s tax bill are moving in opposite directions under the same administration, that isn’t an accident of the business cycle. That’s a preference. A choice.

The one bright spot on the revenue side that the administration will absolutely wave around is tariffs. Customs duties did rise, and rose in a way that’s genuinely visible in the data. But it’s a fraction of what was promised. We were told tariffs would fund tax cuts, pay down the debt, replace the income tax entirely, depending on which month and which speech you caught you might have even heard that we were all getting a check in the mail. A tariff dividend! What actually showed up is marginal increase over historical receipts and we don’t yet have a clean accounting of what those refunds the Supreme Court forced Trump to give importers will do to the back half of this fiscal year’s revenue picture. But it’s coming, and it’s not going to be flattering.

Then there’s the spending side, and this is where “fiscal responsibility” really goes to die. Outside the mandatory, untouchable stuff—Social Security, Medicare, the interest payments nobody can skip—this budget takes a knife to the discretionary services layer. Health and Human Services programs outside the big entitlement trust funds are getting squeezed. And that’s why half the country has diarrhea right now. Thanks RFK! Education funding is getting gutted with the second largest year-over-year cut of 55%. These are the parts of government that show up in a kid’s classroom or a community health clinic, and they’re the ones absorbing the cuts, because they’re the parts of government with the least political muscle to defend themselves.

Here’s the twist, though: for all that reshuffling—soak the individual, ease off the corporation, gut the classroom, feed the Pentagon—the deficit is running on basically the same trajectory it always has. Same order of magnitude. Same structural shortfall between what comes in and what goes out. Nothing about this administration’s approach has bent that curve in either direction in any way that matters.

Which tells you the whole “fiscally responsible” costume the GOP wears is exactly that—a costume. This is one of the great magic tricks in modern American politics: a party that markets itself as the adult in the room, the green-eyeshade grown-up worried about your grandkids’ debt burden, while it runs deficits that look identical to the ones it spent the last administration screaming about as the opposition party. This is the GOP pattern in raw numbers. It’s how it goes, every single time a Republican administration gets the keys—the rhetoric of austerity paired with the reality of unchanged deficits, just reallocated toward the military and away from everyone else.

Now for the really fucked up part: It really doesn’t matter. Someone commented a while back on one of my budget pieces that they were confused because I’m a believer in the concept of modern monetary theory (MMT). So this is as good a time as any to explain why.

The way deficits get discussed in the press, and frankly the way both parties have trained the public to think about them, is clinical and moralistic—like a household budget, like a maxed-out credit card, like a debt that will one day come due and crush us all under the weight of our profligate spending. It’s a neat story. Tidy. It’s also not supported by the evidence.

Since the United States moved to a floating fiat currency, decades of data show no reliable correlation between the size of our deficits and either a debt crisis or runaway inflation. We’ve run large, persistent structural deficits for years at a stretch without the bond market revolting and without prices spiraling out of control. The relationship the deficit hawks insist must exist simply hasn’t shown up in the data over time.

What that opens up is an uncomfortable but important idea: as the issuer of the world’s reserve currency, operating under a sovereign fiat system, the United States is both the engine and the gasoline of the global financial system, and will remain so until the world collectively decides to move away from dollar-based settlement and the petrodollar arrangement. Translation: we don’t just have the capacity to run deficits—in a very real sense, running them is the job. We are the liquidity the rest of the world depends on. But look at how we’ve chosen to exercise that power. We’ve chosen to flood the world with our currency rather than our products. That’s a policy choice, made repeatedly, across administrations, in favor of financialization over production.

And here’s where the priorities conversation gets real. If we took, let’s say, a trillion dollars away from military spending, dollar for dollar, and put it into social programs, education, infrastructure, and healthcare, we would still be the largest defense spender on the planet, by a wide margin. The Peterson Foundation has shown for years that U.S. defense spending outpaces the next several countries combined. So the “we can’t afford it” argument dies on contact with that chart.

The counterargument you’ll hear, usually from people who should know better, including plenty of Democrats who’ve cozied up to this framing, is that military spending is somehow non-inflationary because it doesn’t compete for domestic labor the way social spending does, so it doesn’t create the kind of cost-push inflation that, say, a big infrastructure push would. Again, neat theory. It’s also not true, and never has been. We build weapons in factories staffed by American workers. We pay service members real wages. We cut enormous checks to private military contractors who are, last I checked, companies employing people, just like a bridge-building firm or a high-speed rail contractor would be. What’s the actual cost-push difference between a dollar spent on a missile and a dollar spent on a bridge? None. Zero. It’s the same dollar, moving through the same economy, employing the same category of worker. The only difference is what we’ve collectively—Democrats included—agreed to call “necessary” versus “discretionary.” It’s all discretionary and we just happen to make really bad choices.

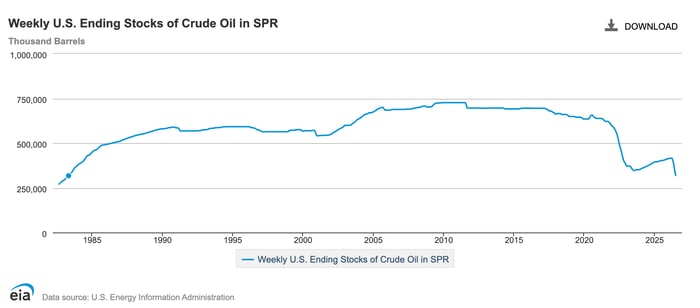

And now the policy chaos of this moment is putting a very literal face on what happens when you spend down the things you spent decades stockpiling. Experts are warning that the U.S. burned through so much of its precision missile inventory trying to topple the regime in Iran that it may not have what it needs for the next conflict, whenever that comes (CNN). Meanwhile, our Strategic Petroleum Reserve—the emergency cushion built for exactly this kind of moment—is sitting at levels not seen since 1983 (EIA). We are quite literally depleting both the ammunition and the energy buffer that a rational government would treat as sacrosanct reserves, in service of a foreign policy adventure with no clear off-ramp. This is chaos, and chaos this scale doesn’t announce its bill up front. It bills you later, in ways you don’t see coming.

But let’s bring it back to the budget, because there’s a point buried in all of this. Government spending, right now, is enormous. We are selling an almost unfathomable amount of debt and running a volume of activity through the bond markets that is genuinely unprecedented in scale. And that volume does something quietly useful for the people running this show: it masks a lot of ugly indicators underneath it.

All that money sloshing through the system pads the wallets of traders, custodians, clearing houses—everybody taking their nip here, their tuck there—while keeping the capital circulating within the financial system itself, rather than reaching the parts of the economy that are slowly being starved. That can’t go on forever. Nothing built on that kind of imbalance does. But the next time someone tells you the government “can’t afford” a program, remember what this statement actually shows: the top line and the bottom line haven’t moved all that much. What’s changed is what’s written in the lines in between—and that’s where the priorities live, in plain sight, for anyone willing to read the ledger instead of the press release.

Running Dry

Here’s a look at the stockpiles we mentioned above.

Source: eia

According to Reuters, “The drawdowns are a part of a U.S. agreement to release 172 million barrels from the facility. Since the U.S.-Israeli war on Iran began at the end of February, SPR inventories have fallen by 98.9 million barrels as of July 10.”

We’ve discussed the many reasons why oil prices have been contained relative to the physical shock but we’re fast approaching the point where even the traders won’t be able to manipulate them. At some point the United States is going to have to increase output for our own reserves, which means we won’t be able to be the release valve for Europe that we have been for months. Analysts also predict that China is soon to come roaring back into the market after depleting its stockpiles. Stockpiles, mind you, that were way bigger than anyone realized.

With the renewed fighting and bombing in Iran and the Strait of Hormuz, it’s highly unlikely that anything but Iranian-approved oil will escape this chokepoint for the foreseeable future. So the other pipelines and waterways that have absorbed the shock will have to continue to do so in the months and maybe even years ahead. Basically what we’re looking at is a world that is going to drive a staggering amount of demand for oil through fewer channels all at once. Apart from the supply chain issue, the bigger problem freaking out the industry is that the world simply doesn’t have the capacity to refine products at the anticipated volume.

Traders have done their part with the hand they’ve been dealt and kept oil relatively stable, albeit elevated since before the Iran war. But fundamentals are fundamentals and at some point they just take over.

Max is a political commentator and essayist who focuses on the intersection of American socioeconomic theory and politics in the modern era. He is the publisher of UNFTR Media and host of the popular Unf*cking the Republic® podcast and YouTube channel. Prior to founding UNFTR, Max spent fifteen years as a publisher and columnist in the alternative newsweekly industry and a decade in terrestrial radio. Max is also a regular contributor to the MeidasTouch Network where he covers the U.S. economy.