%20Over%2c%20Humanoids%20Are%20Dumb.%20Consumer%20Sentiment.%20UNFTR.jpg) Image Description: On The Record 5-26-26. The AI Black Hole: OpenAI, SpaceX and Anthropic. The War Is (Not) Over, Humanoids Are Dumb. Consumer Sentiment. UNFTR

Image Description: On The Record 5-26-26. The AI Black Hole: OpenAI, SpaceX and Anthropic. The War Is (Not) Over, Humanoids Are Dumb. Consumer Sentiment. UNFTR

All for Them. None for You.

We’re going to talk about AI and the stock market today. Not for investment purposes or to try and predict something, but to illustrate the severity of capital concentration risk in the United States economy. Money makes the world go ‘round, and right now it’s being sucked into a gigantic black hole with no guarantee that it’s coming out the other side. This has real-world consequences for us all.

Before we dive in, there are three concepts you need in your pocket before we get into it: Initial Public Offering (IPO), Valuation, and Market Capitalization. If you’re not in the investment world, these are just words you probably hear floating around in the ether. They’re not complicated, just important to the context of a rather astounding development.

An IPO is the moment a private company sells shares of itself to the public for the first time. Before that moment, ownership is limited to founders, employees, and private investors (venture capital firms, sovereign wealth funds, wealthy individuals, etc). After the IPO, anyone with a brokerage account can buy in.

Valuation is what the market—or in the case of a private company, its investors—believes the entire company is worth at a given moment. It’s not based on what the company has earned. It’s based on what people believe it will earn. Which means it is, by definition, a bet on the future.

Market Cap is the total dollar value of all a company’s shares combined. If a company has 100 million shares outstanding and each share trades at $10, the market cap is $1 billion. It’s the simplest shorthand for a company’s size as the market sees it. When people say Apple is a $3 trillion company, they mean its market cap is $3 trillion.

Three straightforward concepts to level set because 2026 is shaping up to be unlike any other year in the history of public equity markets—driven not by hundreds of companies across dozens of sectors, but by just three IPOs, with valuations that strain credulity and market caps that have no historical precedent.

Moving forward, keep this number in your head: $200 billion dollars. That’s roughly the combined amount that OpenAI, Anthropic, and SpaceX are expected to raise if all three manage to list in the same calendar year, which is looking increasingly possible. And that’s assuming they each sell only about five cents on the dollar of their total value to the public. Companies this large don’t sell themselves wholesale at IPO. They float a small slice, typically 5–10% of total shares, retaining the rest for founders, employees, and early investors. Five percent of a trillion-dollar company still generates tens of billions in a single offering.

And that single figure could exceed the total proceeds raised by every U.S. IPO with a market cap above $50 million from 2022 through the first quarter of 2026, combined. Four years of the American IPO market, swallowed whole by three companies in one year. That is not a prediction about the future of the economy. That is a description of what is already in motion.

Comparables

The concentration of capital flowing into artificial intelligence is not just a story about big numbers. It’s a story about a fundamental reorientation of where investment goes in the American economy, and who gets left out of it.

For most of the past two decades, total U.S. R&D spending across all sectors—private industry, federal government, universities, nonprofits—ran at roughly 3% of GDP. In dollar terms, that meant somewhere between $400 billion and $700 billion annually by the early 2020s, spread across thousands of companies, research institutions, and sectors: pharmaceuticals, aerospace, automotive, agriculture, energy, materials science, defense, software.

The National Science Foundation put U.S. gross domestic R&D expenditure at $923 billion in 2022. Enormous, yes. But broadly distributed. A pharmaceutical company developing cancer treatments, and a university lab studying soil microbiomes, and a defense contractor working on propulsion systems all drew from the same general ecosystem of capital, talent, and institutional support.

Now look at what has happened in the past two years.

The four largest hyperscalers—Amazon, Google, Meta, and Microsoft—spent $443 billion on infrastructure in 2025 alone. Goldman Sachs projects total ecosystem-wide AI capital expenditure (CapEx) of $765 billion this year, scaling to $1.6 trillion annually by 2031, and $7.6 trillion cumulatively through the end of the decade. Amazon alone is committing $200 billion this year, a figure that will push it to negative free cash flow. The hyperscalers, to fund this, raised $108 billion in debt in 2025 alone, with projections of another $1.5 trillion in total debt issuance over the coming years.

This is what concentration risk looks like. The entire historic R&D ecosystem is being eclipsed by a single-sector buildout controlled by a handful of private and semi-private entities. And if we talk about the three companies on the IPO slate we’re talking about Sam Altman, Dario Amodei and Elon Musk. The New Yorker profile of Altman basically confirmed that he’s a pathological liar and a sociopath. Amodei has said in nearly every interview that he thinks AI is going to destroy us. And Elon Musk tried to dismantle the U.S. government. This all sounds fine! Anyway, back to R&D.

The WIPO Global Innovation Index 2025 found that global R&D growth slowed to just 2.9% in 2024 and is projected to fall further to 2.3% in 2025—the weakest expansion in over a decade. Goldman Sachs noted that traditional industries “have been starved of capital spending” since the Global Financial Crisis, and the AI buildout has deepened that trend because hyperscaler spending stays within the AI infrastructure ecosystem rather than flowing outward into the broader productive economy. AI boosters will argue that this is normal, and in fact, necessary, because AI is going to supercharge innovation on behalf of these sectors. It’s a point worth arguing, but we should be clear that this remains entirely theoretical.

Then there’s the public side of the ledger, where the retreat is deliberate. The Trump administration’s FY2026 budget proposed a 22% cut to total federal R&D, including a 36% cut to non-defense R&D specifically. The NSF faces a 56% reduction. The NIH faces 43%. The Department of Energy, 31%. Nature reported that after adjusting for inflation, the proposed decrease in non-defense research funding would roll spending back to 1991 levels. Congress has blunted the worst of it in enacted bills, but thousands of active grants have already been cancelled or suspended, and the structural damage to university research pipelines is already underway.

Which brings us to 2026, and what may be the most consequential IPO season in the history of financial markets.

In a normal, healthy IPO year in the U.S., somewhere between 150 and 250 companies go public across a wide range of sectors: healthcare, industrial, consumer, technology, energy, financial services, real estate. The dot-com peak of 2000 saw 406 U.S. IPOs. The 2021 SPAC boom generated 1,035 offerings. We were on pace for a healthy IPO season this year, but things have slowed down as the Iran war drags on and uncertainty abounds.

The number of filings is less interesting than the valuations that we’re seeing in AI. To give you a sense of comparable offerings that are familiar to most, Facebook listed at $81 billion and Uber at $75 billion.

Contrast these with SpaceX, which is targeting a valuation of $1.5 trillion at listing—nine times the size of the largest American IPO ever. OpenAI is preparing to file S-1 documentation in the coming weeks, per the New York Times, with a target valuation of $850 billion to $1.1 trillion. Anthropic, currently valued at $380 billion in the private market following its February Series G, is being discussed at $850 to $900 billion at IPO, with bankers suggesting the offering could raise more than $60 billion.

Combined, these three companies represent approximately $3 trillion in prospective market capitalization. To put that in context: that’s roughly the size of France’s GDP.

And the sectors represented? Artificial intelligence and rockets. That’s it. No healthcare breakthroughs. No new energy companies. No consumer brands, no industrial innovators, no agricultural technology, no materials science. Three companies, one technology wave, a narrow slice of humanity’s productive activity—absorbing capital that in any previous era would have been distributed across hundreds of firms and dozens of sectors.

What This Means

The question isn’t whether these are transformative companies. It’s not even whether they’re good companies. The question I’m asking is a different one: who owns the upside?

When Facebook went public in 2012, any American with a brokerage account could participate on day one. The democratization of equity ownership—imperfect, unequal, but real—has historically meant that transformative wealth creation at least partially flows back into the broader economy through retirement accounts, pension funds, and public market participation.

The IPOs coming down the pike look different. Every company that goes from private to public has a group, or several groups of preferred investors that put in early money and expect a larger payout for taking a risky position. The difference with these companies is that they’ve already taken in such enormous sums of investment capital through multiple rounds and secondary market trading that they’ll be the true beneficiaries of compounding returns before a single retail share ever trades.

OpenAI CFO Sarah Friar has confirmed that retail investors will get an allocation. But the bulk of the value creation—the distance between early private valuations and eventual public price—has already accrued to a very small group of venture funds, sovereign wealth funds and strategic corporate investors.

The $725 billion in hyperscaler CapEx this year, the $7.6 trillion projected through 2031, the $3 trillion in IPO market cap bearing down on public markets; all of it is being built on a narrow foundation. A handful of chips, most of them manufactured in Taiwan. A handful of companies. A handful of investors. A handful of decisions, made in San Francisco, Riyadh, Abu Dhabi and a few rooms in Washington DC.

It’s not a conspiracy, it’s a structural observation. Capital concentrates, and it always has. But the velocity and the scale of capital concentration at a time when public R&D budgets are being slashed and social safety nets are being cut is like nothing we’ve ever seen before.

In other words…All for them. None for you.

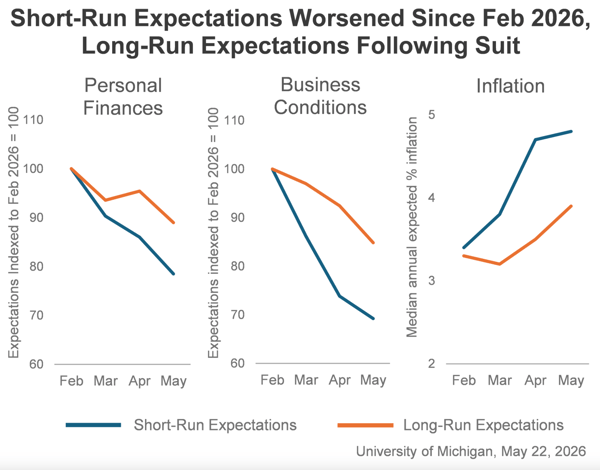

When Sentiment Is Reality

Consumer sentiment is the lowest it’s ever been. According to the Michigan data that came out at the end of last week, the numbers have fallen off a cliff as inflation continues to gobble up wages and savings. From the report:

“Sentiment is now just below the previous historical trough seen in June 2022. The cost of living continues to be a first-order concern, with 57% of consumers spontaneously mentioning that high prices were eroding their personal finances, up from 50% last month. Lower-income consumers and those without college degrees posted particularly strong sentiment declines; these groups are more sensitive to increases in the cost of gas and other essentials.”

Source: University of Michigan

The short-run expectations make sense given the immediacy of gas prices. It’s a shock to the system to see prices creep to $5/gallon and in some cases beyond. The fact that the long-run is cratering in tandem and to such a significant degree is the visualization of reality setting in. It’s the end of May. The time stamp that every talking head on TV and economist has referenced as the point of no return for 2026. No matter what happens with these on again/off again “negotiations” with Iran, we can kiss any growth expectations for 2026 goodbye.

Max is a political commentator and essayist who focuses on the intersection of American socioeconomic theory and politics in the modern era. He is the publisher of UNFTR Media and host of the popular Unf*cking the Republic® podcast and YouTube channel. Prior to founding UNFTR, Max spent fifteen years as a publisher and columnist in the alternative newsweekly industry and a decade in terrestrial radio. Max is also a regular contributor to the MeidasTouch Network where he covers the U.S. economy.